What is a Mutual Fund?

When speaking about investing, a common term you may have heard is a “Mutual Fund.” A mutual fund is a type of investment that pools money from many investors and uses it to invest in a variety of different assets (such as stocks or bonds).

Rather than using your money to purchase just one share of a company, you can invest in a mutual fund that would provide you with a small piece of multiple assets. Mutual funds are a great way for investors to diversify their portfolios and mitigate risk. It is important to remember that, although you do not directly own the shares of the company, you will share in the profit or loss of the underlying security.

All mutual funds serve a different purpose, and each one has unique benefits to the investor, such as diversifying your asset classes, investing in a multitude of companies, tracking an index, or tacking a specific retirement year. When trying to decide which fund you should invest in, we always recommend speaking with a trusted financial professional to explore all of your options.

Are Mutual Funds Right For Me?

If you are wondering if mutual funds are a good choice for your portfolio, you should first figure out what your approach to investing is. If you are looking for a passive investment, you may consider investing in an index fund or a mutual fund that tracks the S&P 500 index.

This is a good choice if you are going with a “buy and hold” approach and hope to perform to market historical standards. If you are looking to be more of an active investor and try to outperform the market, this may not be the choice for you.

Another option would be to use a mutual fund that is actively managed with an assigned account manager, who is making decisions on what securities within the mutual fund to buy and sell regularly. The main downside to this option is that the mutual fund will likely have a higher fee, but typically can have higher returns. Keep in mind, it is difficult to outperform the market and there is no guarantee that the actively managed fund will yield better returns.

Many people feel more comfortable using a mutual fund with an active account manager, as it brings peace of mind that their investments are being managed by a professional with experience, and consistently in line with their investment goals and approach.

Types of Mutual Funds

There are many different types of mutual funds to choose from, each providing a different benefit and can all be useful to have in your retirement portfolio.

Equity Funds

An equity fund is a mutual fund that primarily invests in stocks, which can be useful for diversifying your portfolio. Rather than investing in just one large-cap stock, you can invest in hundreds of stocks. These are a great way to get started on your investment journey if you lack the time to research hundreds of different individual companies. Equity funds typically have some type of account manager that is buying and selling the stock within the fund (in turn doing the research for you).

Money Market Funds

Money market funds provide the lowest risk of all mutual funds, as they invest in short-term securities, such as government-backed securities like treasury bonds and Certificate of Deposits (CDs). If you lack confidence in the short-term market, it may be wise to invest in money market funds to keep your portfolio safe from down-turns. Although you should be cautious, low risk typically translates to low returns.

Index Funds

An index fund is another example of a passive investment vehicle. These funds typically try to mimic the performance of a financial index like the S&P 500. The fund manager may exclusively purchase stocks from the S&P 500 for the index fund, which would allow you to mirror the entire index without actually shelling out the money to buy shares in each company.

Balanced Funds

A balanced fund (as the name would suggest) is a balance between stocks and bonds that can allow investors to diversify their asset classes between debt and equities. This is great for more conservative investors, or those nearing retirement age who are looking for a low-risk investment that may yield more than a money market fund. This is designed to be the sole investment in your account.

Target-Date Funds

A popular choice for retirement plans is the target date fund. This fund works by selecting a specific retirement year (for example, 2055) and updating the underlying securities (mix of equity and fixed income) to reflect that date. If you are using it for retirement, you would select the date fund closest to your anticipated retirement age and the fund will reduce risk in the portfolio as you get closer to the set date. This is helpful for passive investors who do not want to actively manage a portfolio but would like to gradually reduce risk. This is designed to be the sole investment in your account. Although you should be cautious, Target-Date Funds may take more risks than you are comfortable with. Be sure to do your research to understand how the recommended fund is being managed.

Income & Growth Funds

An income fund is a type of mutual fund that seeks to provide income to the investor through dividends or interest payments. This fund differs from a growth fund as the income fund will pay dividends back to the investor in cash while the growth fund will re-invest the money back into the fund which helps it grow over some time.

Choosing the Right Mutual Fund

With all of the options we just explored, you may have more questions than answers. You may be wondering, “How do I choose which mutual fund to purchase?” Totally valid. There are a few ways to ensure that you are making the right decision:

1. Research– Start by researching the fund you are interested in. You should always fully understand your investments to mitigate risk. Look at the mutual fund’s past performance to see how it has performed in the last year and 5 years. You should take into consideration how long you expect to hold the fund. If you are expecting to hold it for 10 years, then look at the 10-year performance and compare it to that of other funds.

2. Evaluate Your Goals- Determine what benefit is most important to you when it comes to investing. If lower fees are more attractive to you, then you may prefer an index fund over an equity fund. If you are more risk-averse, you may gravitate to a money market fund or balanced fund. If you are looking for a source of additional income, an income fund that pays dividends will be your best bet. Regardless of what you choose, it should be in line with your retirement goals before you make the purchase.

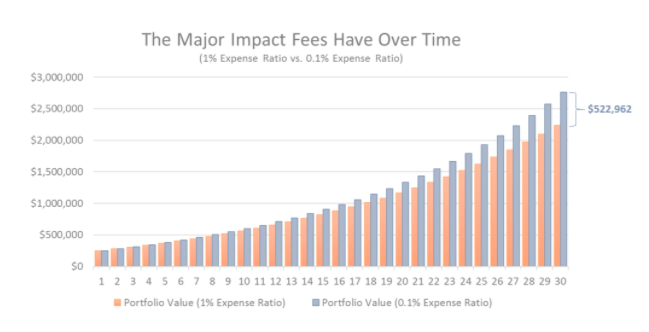

3. Check the Expense Ratio- Every mutual fund will have a different expense ratio. This is the fee to the investor for the convenience of having a mutual fund that covers the fund’s expenses. The following infographic illustrates how an expense fee of 0.1% versus 1% can have a significant impact on your lifetime portfolio value (a difference of $522,962).

Source: ModelInvesting

With all of the options available, it can feel intimidating and tough to decide. All investment decisions come with their pros and cons. It is always a good idea to do your research and consult with a financial professional, such as Artesys, when making any major changes to your portfolio. Artesys works in your best interest to deliver a one-of-a-kind managed account solution with a 20+ year track record.

Stay informed

Sign up for our monthly newsletter and take control of your financial future.